About the survey

The survey was carried out by Williams & Co, the UK’s largest independent Plumber’s Merchant in order to gain insight into the financial and emotional impact of the lockdown, and to explore potential future options.

Data was collected over the bank holiday weekend 8th to 10th May 2020. All responses were gathered before the Prime Minister’s speech on the evening of 10th May.

Who Participated?

This survey is overwhelmingly the story of the self-employed and micro-businesses and their response to the COVID 19 outbreak. Participants were recruited to complete an online survey via email, social media, and SMS campaigns. 1,388 individuals started the survey, of whom 1,151 (83%) completed it.

More than half of the respondents were “one-man-band” businesses, and 92% of respondents worked for firms with 5 employees or fewer. The commonest areas of work undertaken by participants were “Domestic plumbing repairs and maintenance” (83%), “Gas or oil boiler installations” and “Boiler servicing and repairs” (both 75%) and “Bathroom installation” (63%).

What does the survey tell us?

After a couple of questions designed to learn about the respondent, the survey dived straight into the heart of the issue with this question:

Have you been working during the lockdown period?

Just over a quarter of respondents reported not working at all. Nearly a fifth have been attending emergencies only, and 31% have worked in low-risk environments, like empty buildings as well as attending emergencies. 18% have continued to work as normal, with varying degrees of precautions, so long as the customer wanted the work to go ahead.

Of those not working, the most common single reason given was that there was no work to be done, with “personal choice” as the second most frequent. Only 3% of all respondents were on furlough, although the “other” category included a range of personal reasons for not working – including shielding, living with individuals in high-risk categories, difficulties with childcare arrangements, and the strongly held sentiments of family members.

Four respondents reported not working due to having suffered from the virus themselves.

Our next question focussed on how respondents would approach life after lockdown:

What are your plans for after the lockdown is lifted?

3% of people have no plans to return to work in the near future, nearly 2% plan to leave the industry altogether, and for employees, much will depend on their employers’ approach. Nearly 7 out of 10 plan to get back to normal working as soon as possible, with a significant minority (23%) taking a more staged approach to returning to work.

Part of the reason for undertaking the survey was to inform ourselves and the rest of the merchant industry about what will be expected of merchants in the coming months. Is the COVID-19 outbreak going to change the way that merchants and their customers interact? The next few questions addressed this issue:

Once lockdown is over how will you want to place orders for materials?

Although there is strong interest in online purchases, it looks like the trade counter is going to retain its importance in the coming months, with over 70% expecting to visit merchant premises. When we forced respondents into a single choice with the next question, the trade counter remained stubbornly popular, although only slightly ahead of the combined digital options.

If the trade counter is still going to be at the heart of the relationship between trade customer and merchant, then it is important to ensure that this can be managed safely.

Providing hand sanitiser and restricting numbers in store were neck and neck for the preferred safety measures. For the 5% who ticked the “other” box, the commonest sentiment was that all such measures are disproportionate or unnecessary, although several respondents didn’t think that the options mentioned went far enough.

Finally for this section – we addressed the thorny topic of handling cash.

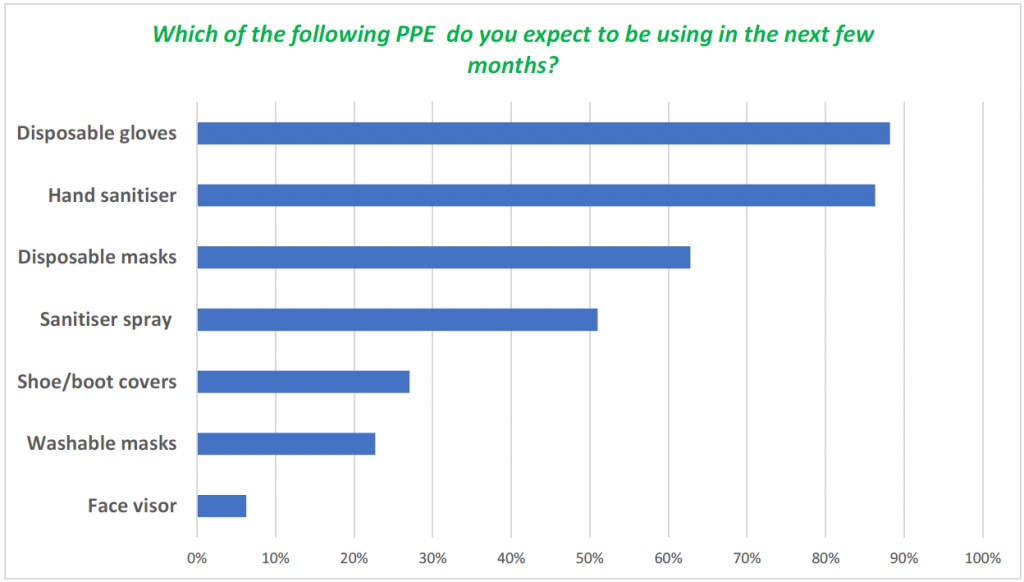

In terms of precautions that tradespeople were taking themselves, we asked what PPE they were expecting to be using in the coming months.

Unsurprisingly, it looks like the manufacturers of disposable gloves and masks, and the makers of sanitiser gels and sprays can look forward to a bumper year:

Sharing vehicles – whether in vans or on public transport – seems to be a potential opportunity for the virus to spread. Given the nature of the occupation, we were not shocked to learn that just 3% of tradespeople use public transport either to commute or as part of their working day. However, it seems that at around one third of respondents do expect to be sharing a vehicle at least sometimes.

Financial Impact

Moving away from the practicalities of returning to work, the survey addressed the financial impact of the lock-down.

There is a range of government schemes to assist the self employed and small business, including the Coronavirus Job Retention Scheme (CJRS), the Self Employed Income Support Scheme (SEISS), Bounce Back Loans Scheme (BBLS) and the Coronavirus Business Interruption Loan Scheme (CBILS). Since BBLS and CBILS are mutually exclusive and do the same job for different businesses, we treated them jointly. The timing of the survey meant that it was likely that many applications for help would still be in progress, or at the eligibility checking stage. Options were provided for “in progress” applications.

Although the biggest reason for a given scheme not helping was that its eligibility criteria didn’t apply to a particular situation, a substantial number decided not to apply for BBLS or CBILS even if they felt that they could have qualified.

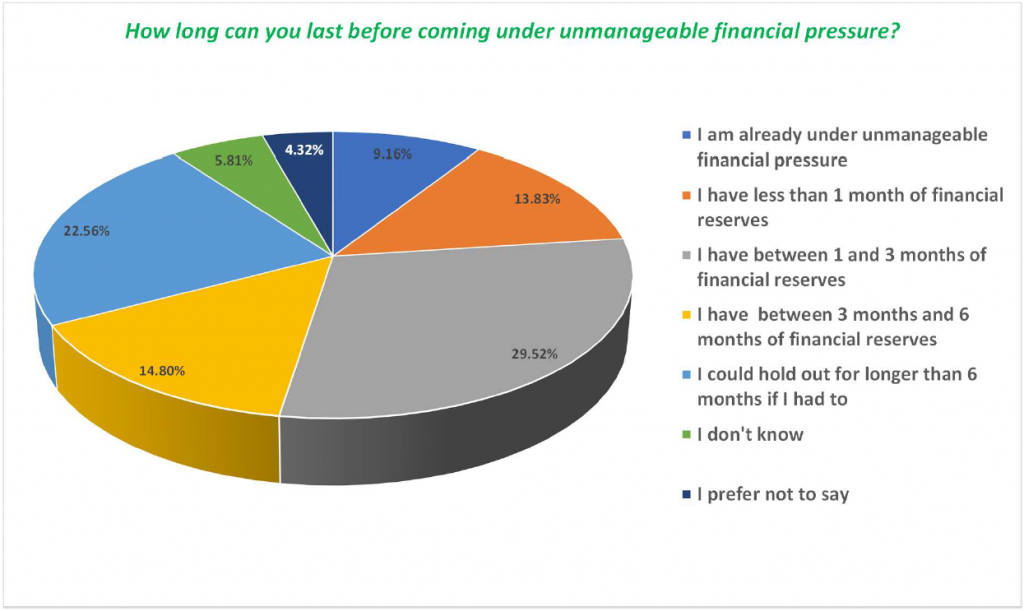

In the longest question in the survey, we asked: “Assuming that business continues at the current rate, and taking into account savings, reserves and any help that you are receiving or expect to receive from any of the schemes mentioned, how long could you last before coming under unmanageable financial pressure?” For nearly a quarter of those participating, that moment has already come, or will come in the next month. Approximately the same proportion are well placed to ride out the storm, with others somewhere in between, or keeping their own counsel.

The financial cost is not the only measure of the impact, and the last multiple-choice question on the survey sought to understand more about the pressure put on emotional and mental health.

In addition to the quantitative questions described above, there were nearly 1,500 free-format text responses to questions about the way that merchants and trade bodies have supported their customers and members. The sheer scale of these comments will require some time to analyse, but at first glance most comments about merchants have been neutral or positive. Sentiment about the help provided by trade bodies, particularly Gas Safe, has been less upbeat.

Thanks to all those who contributed their responses.

Ray Stafford

10th May 2020